For most of the last decade, the binding constraint on European renewable build-out was capital and capacity — money and megawatts. From 2022 onwards, in a growing number of markets, the binding constraint is the grid.

It is worth being precise about what “the grid” means here, because it has become a constraint on both sides of the meter. On the supply side, new generation waits in connection queues measured in years and energises into networks that cannot yet fully evacuate it. On the demand side, the large flexible loads that would absorb that generation — data centres above all, alongside electrolysers and electrifying industry — are themselves stuck in connection queues, arriving late and often in the wrong place. The result is a timing and locational mismatch between where power is produced and where it can be consumed. Its visible symptoms are the two that now dominate every revenue model: negative-price hours and curtailment.

Most of the offtake structures in recent years were drafted in the capital-and-capacity world. They now need to be retrofitted for the connection-constrained one. This matters because the failure mode is asymmetric. A connection-constrained PPA does not fail at signing. It fails in year two — when the asset energises into a curtailed local market, or has its commissioning delayed past the contractual cover.

A connection-constrained PPA does not fail at signing. It fails in year two.

The data has already turned

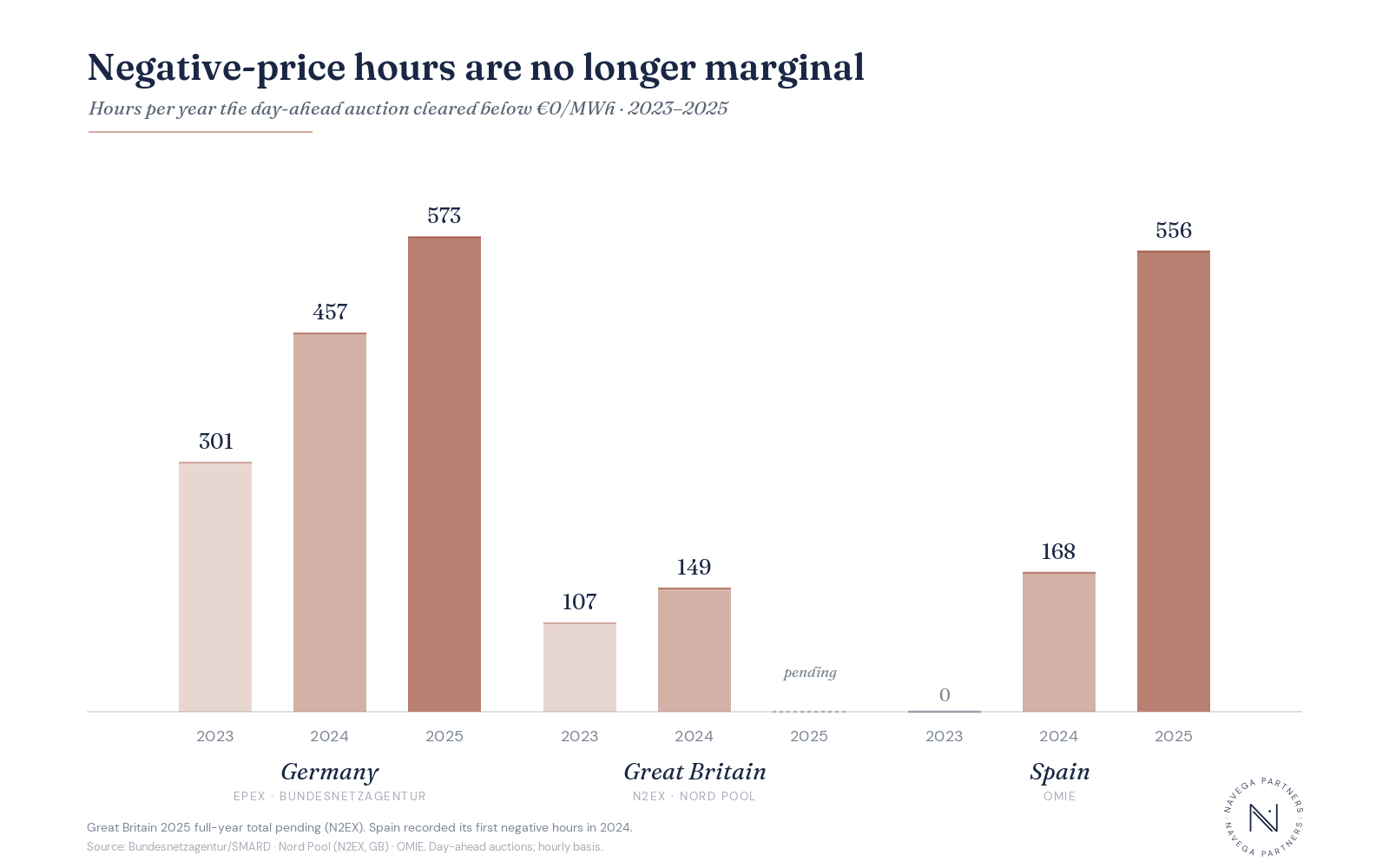

This is no longer a forecast. The clearest single indicator is the number of hours each year in which the day-ahead auction clears below zero — the market paying to be relieved of power it cannot place. The operators’ own figures show the inflection.

Two features of that record carry the argument.

First, the trend is unmistakable and recent. Germany has gone from 70 negative hours in 2022 to 573 in 2025. Great Britain, on N2EX, rose from 107 hours in 2023 to 149 in 2024, with 2025 shaping up as another record. Spain, which had never recorded a negative day-ahead hour, logged 168 in 2024 — its first year of the phenomenon — and more than tripled that in 2025. This was a marginal drafting consideration five years ago and is a central commercial term today, and the acceleration has not stopped: Iberia is carrying the trend further still into 2026.

Second, the constraint wears a different face in each market. Where the price mechanism is granular enough to express oversupply, it shows up as negative prices. Where it is not, it shows up as curtailment volume and cost. In 2024 the United Kingdom curtailed more than a tenth of its wind generation, around 8 TWh, at a transmission constraint cost approaching £1.9bn in 2024/25 (National Grid ESO / NESO) — most of it Scottish wind the network cannot move south. Spain’s curtailment of wind rose from a fraction of a percent of output in 2022 to several percent by 2024, and on the worst summer days of 2025 the system spilled close to 11% of all renewable generation (Red Eléctrica / REE). Germany manages a far larger volume again through redispatch (Bundesnetzagentur). Italy has barely seen a negative day-ahead price, yet faces the same problem as volume, concentrated in the generation-heavy South behind the bottleneck to the demand-heavy North. Same constraint; different meter.

Three structural shifts

Curtailment moves from the margin to the centre. In a 2020 PPA, curtailment was usually allocated to the producer by default — a residual exposure small enough to sit inside the merchant case. Allocated the same way in 2024, in the same market, it is no longer residual. Once a node spills several percent of output in its worst months, the producer is carrying a volume risk large enough to move the project’s bankability, and a lender will now price it as such.

The locational question becomes contractual — but not in the way most contracts assume. This is where the most common drafting error sits, because the instinct is right while the mechanism is widely misunderstood. Continental Europe and Iberia price by bidding zone, not by node: within a zone, every plant clears at the same day-ahead price regardless of location, and intra-zonal congestion is resolved by the system operator through redispatch and curtailment. So the locational risk in a European PPA rarely shows up as a price gap between the plant and a hub. It shows up in three other places — the shape (or profile) difference between pay-as-produced volume and the baseload product that most buyers hedge against; the cannibalisation cost of a generation profile that increasingly clears at or below zero in the very hours it is largest; and, for cross-border structures, genuine basis between bidding zones.

Commissioning risk has lengthened. The connection queue and the upgrade schedule together mean a project signed in 2026 may not energise until 2028 — and, increasingly, that when it does, it energises on a constrained or non-firm connection, exporting below nameplate until the relevant network reinforcement clears. Availability guarantees and ramp-up clauses already handle the asset’s own commissioning curve; what they were not built to catch is a grid-driven export limit that can persist for years after the plant itself is ready. The standard cover for delay — liquidated damages capped at a percentage of contract value — was calibrated for shorter slips, not for a multi-year reinforcement timetable, and still less for a project that meets its commercial start date on paper but not in megawatts.

What structures absorb the constraint

The structures that hold up in this environment share a few features. Some are already standard practice; others are at the frontier of what is being negotiated, and it is worth being honest about which is which.

They allocate curtailment explicitly and proportionally: a defined threshold below which the producer absorbs the cost, above which it is shared, and at the extreme a defined renegotiation window rather than a unilateral exit. Increasingly they also specify how negative-price hours are treated — for example, suspending payment when the day-ahead price sits below zero for a defined run of consecutive hours. There is even a regulatory template for the mechanism: Germany’s “six-hour rule” withholds subsidy support from larger plants once the day-ahead price is negative for six or more consecutive hours, tying the trigger to a defined, observable condition rather than a discretionary judgement. This is established ground.

They price the locational question rather than treating it as a logistical footnote: shape, cannibalisation and any cross-zonal exposure built into the contract economics rather than left as an off-balance-sheet surprise for whichever party is least able to see it coming. Pricing these in is now standard. The harder design question is what to do with an exposure that genuinely cannot be hedged — and here the honest answer is that the options run from an explicit risk premium to a narrowly bounded review trigger, the latter used sparingly, because an open revisit right is exactly what a lender will not fund.

They treat commissioning as a sequence rather than a single date. Milestone-based commercial-operations dates and longstop dates are already standard; what the connection-constrained world adds is a tighter interface between the PPA and the grid-connection and construction milestones beneath it, so that the delay and liquidated-damages structure flexes across staged capacity — first export, grid-code compliance, ramp to nameplate — rather than collapsing onto a single trigger.

And the most demanding of them build in a defined recalculation for the operating period: if the asset comes online into a structurally curtailed environment, the parties have agreed in advance how the terms adjust against a stated, observable trigger. This one is not yet standard practice, and it sits in real tension with bankability — lenders resist anything that reads as open price risk — which is precisely why, where it appears at all, it has to be a narrow, formulaic recalculation rather than a re-opener. It is the frontier of the current drafting conversation, not the norm.

Where the work lands

None of this is new finance. It is drafting, modelling and structuring work — the kind that compounds across deals, and that single transactions handled in isolation tend to get wrong. Corporates writing these contracts for the first time tend to under-resource it; producers signing them often assume the structuring gap will be caught downstream, by advisers whose mandate was never scoped to catch it.

The structures that hold up today look meaningfully different from the 2022 vintage. They carry more explicit operational triggers, more defined market-reset windows, and a different liquidated-damages calibration. They take longer to negotiate — and they hold through their tenor, particularly through the second and third operating years, which is precisely where the data above is now putting the earlier vintage under strain.

A grid-constrained Europe is the structural condition, not a passing one, and the offtake architecture has to catch up to it. Increasingly, though, the most durable response is not a better-drafted PPA alone but a more flexible one — pairing intermittent generation with storage so that output can be moved out of the oversupplied hours and into the ones where demand, and price, actually peak, and, where the battery sits behind-the-meter, absorbing local generation that would otherwise be curtailed. Flexibility is becoming the solution driver in this landscape, and it brings contracts of its own — tolling/floor, TBx spreads, optimisation and hybrid-offtake structures — that demand the same explicit triggers and honest risk allocation as everything above. The constraint is rewriting not only how offtake is priced, but what sits behind it.